A Market of Stocks Not a Stock Market.

Why everyone is so over the recession and investing today

Summary: What recession? Not right now please. Market indices climbed higher last week leaving bank defaults, consumer concerns, and earnings season in the rearview mirror. Consumers and cash are still plentiful but retailers say shoppers are focused on the essentials only. Fed chair Powell is following December’s playbook and indicated rate hikes will pause until further notice. Going forward all eyes are on the consumer but at this point the market’s bias is up.

Just the Bare Necessities Please

Walmart

Walmart executives were surprised by the resilience of consumers as they reported financial results beating expectations (earnings per share (EPS) of $1.47 on revenues of $152.3 billion. That topped the expected $1.32 and $148.76 billion). They even guided higher revenue for next quarter.

What is driving the strength? Groceries and essentials. 🛒

Persistently high prices on everyday items are leaving consumers with less discretionary income. And although consumers are still buying higher-margin merchandise, they typically wait for sales to do so.

Economic weakness would suggest a strain on the consumer, but consumer resilience has surprised Walmart execs. They believe that’s in part due to healthy consumer balance sheets.

Same Story From Other Retailers

We saw this pattern in other retailers that reported this week:

Home Depot - Consumers are pulling back on discretionary purchases and instead spending more on necessities. And when they do spend discretionary income, it’s going towards travel, dining out, and other experiences instead of home goods.

Target - Beauty, food and beverage, and household essentials were areas of growth.

Foot Locker - An example non-essentials. Sneakers are NOT necessities. The stock dropped 34% after earnings!

A Market of Stocks, Not a Stock Market

Summary: Opportunities will continue to emerge in specific sectors or themes in the market. Timing them however will not always be easy. AI and Banking will continue to move (up or down) due to external forces.

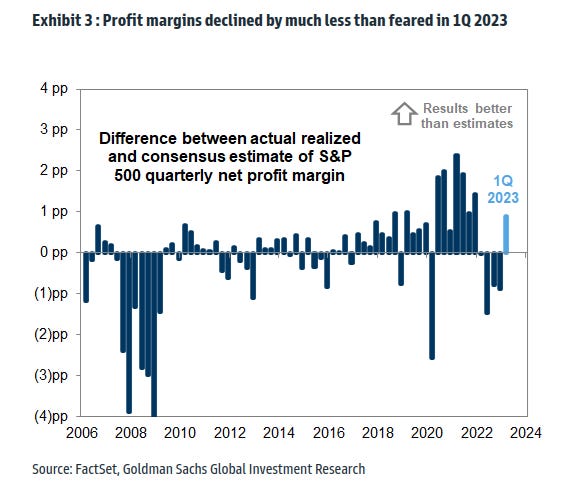

Despite all the doom and gloom going to into the earnings quarter, companies profit margins were less than feared. Investing is all about expectations and when everyone gets so focused on one outcome, the market seems to surprise in the opposite direction.

This earnings season, profit margins declined less than expected. Goldman highlighted earnings stabilized partially because of “resilient revenues, slowing input cost inflation and a weakened USD”.

Multi-billionaire investor Paul Tudor Jones said the economy could enter a recession in the third or fourth quarter, he’s expecting that stocks will end the year higher. “I’m not rampantly bullish because I think it’ll be a slow grind,” he said.

It is a market of stocks and not a stock market.

There is a saying in Wall Street that the it is a market of stocks and not a stock market. We are entering an era where this is likely more true than ever. Technology, policy, and international supply chains will force winners and punish companies that fall behind.

The most wonderful feature of stock market indices is that they are designed to include winners and drop losers over time - think years. Index makers update these indices every 6 or 12 months. By investing in market indices, patient investors are positioned to take advantage of this design. For those with a more active approach, here are two themes to consider. I have written about them before and they are as important as ever. 👇

AI

AI continues to be a dominant theme. As I mentioned before it is undeniable that we are in a multi-decade trend. Large investors believe AI will continue to make princes and paupers.

Steve Cohen, head of the hedge fund Point 72, said he’s “pretty bullish,” and bears may miss out on a wave of AI opportunities. Fellow billionaire Stan Druckenmiller, head of the Duquesne Family Office, agrees that that AI will lead to a bifurcated market of big winners and big losers.

Banking

We had some positive news last week. Western Alliance surged over 10%, and other US regional banks gained, after a jump in its deposits eased concerns about the industry. There has not been any further blow-ups since the failure of First Republic. There still issues with exposure to commercial real estate and in this weakened credit environment (because the Fed is pulling away money) a bank run is a very real risk.

I still think there is opportunity in this space but investors will need to have the skill to pick winners from a basket of duds and the occasional minefield.

Where to next?

Summary: Markets have been driven up largely by large companies. The buying of large cap stocks might take a breather for a few months. Small cap and mid cap companies may provide opportunity for investors as the economy stabilizes. Powell’s Goldilocks scenario seems possible, at least for the next few months.

The S&P and Nasdaq: Next 3-6 Months

The markets seems little worried about the debt ceiling. They are steady right now. After the debt ceiling is resolved, what catalysts are left to drive the market forward? Investors don’t have anything left on the horizon for the next few months. What does this mean for US stock markets? They could drift higher but investors will need meaningful reasons to continue to invest in more US equities.

The S&P 500 is at the top end of the range that is a year old. On the chart of the S&P 500 ETF (SPY below), the price at the top of the range is roughly around 420. With the end of earnings news, investors may have less appetite to buy more stocks. When the markets march higher, the S&P could move up another 5% to the highs of last March.

A good example of the behavior of breaking these ranges is the Nasdaq ETF (QQQ). On April 27th the QQQ ETF cleared the top of its year long range (top of the green line below) and and it has been up 4% since that point.

The Nasdaq has made an impressive recovery. We will need more than large cap companies to make a contribution in order to run higher. 👇

Large Cap Contribution

The market has been driven up by large cap stocks thus far as these are considered “safer” with the questionable macroeconomic backdrop. Large cap tech also raced higher on AI cheer and improved profit margins (by firing people and cutting costs).

There are two dynamics to watch. 1) Have large caps risen too fast for investors? Will sentiment cool off in the short term? Mid-caps and small-caps are still lagging behind. 2) Do investors start buying the stronger businesses in these groups?

Wage Inflation is Declining

It really is a Goldilocks scenario as Walmart pointed out👆. Wages come down and consumer still strong. And now the Fed “we can afford to look at the data and the evolving outlook to make careful assessments”.

The job market is still mostly robust and households and businesses still have significant savings from the Fed’s money printer. This has more than offset the negative effects of wage growth on consumers. A decline in wages has been more manageable than economists predicted.

Other signs of inflation are cooling but why are we focused on wage inflation? Because 1) the Fed is and 2) this is one of the last signs of inflation to come down.

But the price of goods and services are still high some people will say. True. But these are sticky. The cure for high prices is high prices. Because. High prices provide the incentive for new businesses to produce cheaper solutions. They also drive consumers to eventually say enough is enough and seek cheaper solutions.

There is one other immediate cure. A recession. So are we having one? 👇

Recession Hurricane is Downgraded to Recession Watch

Jamie Dimon, the CEO of JP Morgan, made headlines when he warned of a hurricane.

He eventually adjusted his forecast to storm clouds but CEOs, pundits, and economists insist we are still in recession hurricane season. The recession has been pushed out to happen over the next 12 months.

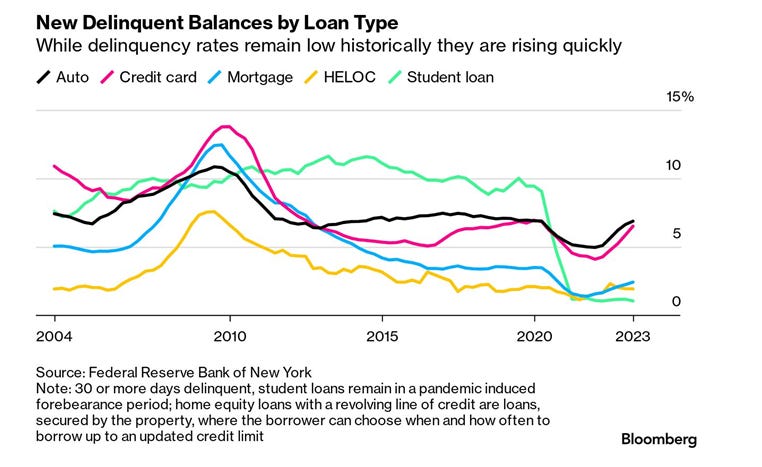

As Walmart executives said, the strength of the consumer is really a welcome surprise. Consumer debt has declined over the last 10 years. In the last few months, credit card and auto debt have started to perk up.

Right now it looks good. If consumers get hit with a financial shock, then debt levels could spiral. To quote Ernest Hemingway debt builds “Two ways. Gradually, then suddenly.”

“How did you go bankrupt?” Bill asked. “Two ways,” Mike said. “Gradually and then suddenly.”

- Ernest Hemingway, The Sun Also Rises

What is this financial shock exactly? Therein lies the mystery of these markets.

If you have any questions, leave a comment. Thanks for reading Embrace the Chaos! Sharing perspective that makes sense.

Much effort and research went into making this 3-minute read. If you found it insightful, please help me out by clicking the like button and sharing this article.

- Vikas Kalra, CFA

A concise but precise and accurate description of the current market situation from a lot of different angles. Loved it! Do you anticipate that the households will face any financial shocks - so that the macro economy is affected in a negative way? Right now consumer spending in essentials is driving growth but can these households, collectively, cause a downward spiral in the economy?