A December To Remember Market

And what you should keep in mind for the future

Summary: Inflation is falling everywhere and markets are rising on expectations of central bank cuts. There is flood of money waiting to be released into the markets in December. Some areas of the market will benefit more than others.

Welcome to the disinflation-everything-rally into year end. Cyber Week prices and the change in prices for CPI and goods are dropping fast. Prices should take 4-5 days to trend sideways in a healthy consolidation. Economic Goldilocks is here (for now). December is setup for a continuing rally and maybe all-time-high in the US and other equity markets.

Let’s review how we got here over the month because the path here defines the future. Then why the rest of 2023 looks bright with holiday cheer. But there is one thing you can’t forget.

Here are the sections to skip around as you please:

💡Retail Companies Still Sounding Alarms

💡Bipolar Consumers or Does Michigan Need Some Sunshine?

💡How Weak Can It Be When Jobs Are So Strong?

💡What This Means For Your Portfolio in December

💡Just In Case You Are Feeling Safe: How It Can All Go Wrong

Your Cheaper Thanksgiving

I hope you all had a great Happy Thanksgiving! Declining price increases have the market giddy.

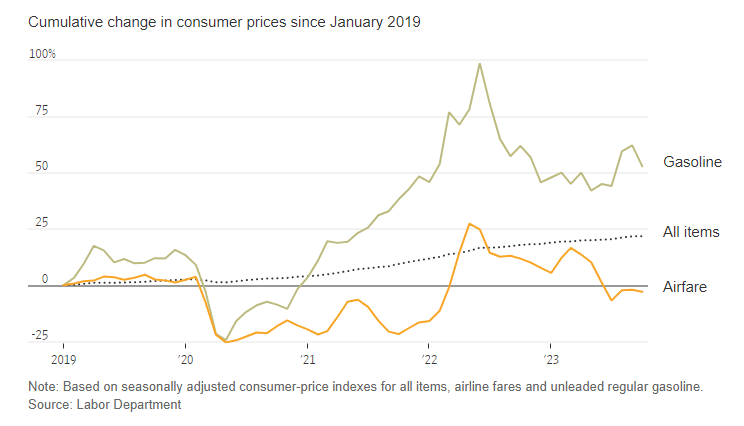

For a start, we can be grateful for future food prices. For most things, price increases have slowed down dramatically. And maybe everything will follow the lowly but mighty potato which is dropping in price.

Holiday travel is getting cheaper supposedly. Transportation prices are showing declines as per the Labor Department (but I am not seeing it when I book tickets for my kids to fly to Disney…I am not sure I agree with this chart).

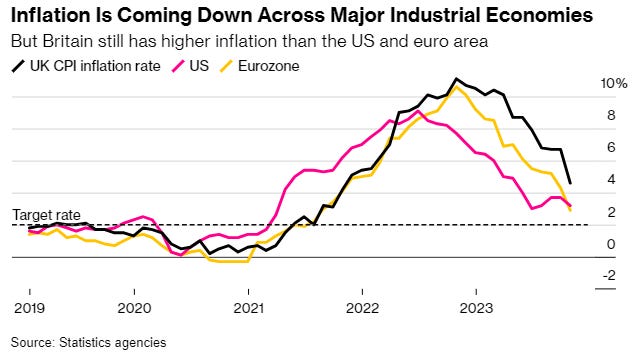

CPI data in November dropped globally with price increases (aka inflation) marching down consistently throughout the year.

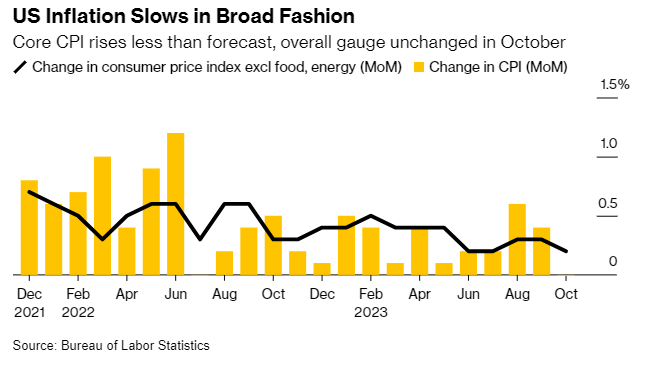

The month over month change in the US Core CPI was nearly 0%! It has been well over a year since that has happened.

The producer-price index (PPI) fell 0.5% in October from the previous month, the largest single month decline since early in the pandemic, according to the Labor Department.

The inflation beast is getting tamed and the market couldn’t be more ecstatic and the holidays couldn’t be more delicious! The biggest implication of declining inflation is expectations of lower interest rates soon (which has a positive impact on equities).

Retail Companies Still Sounding Alarms

That was the macro snapshot, here is some micro (company) level.

We heard from retail companies who are guiding that trouble lays ahead for the consumer. Here are some large retailers.

Target – Barron’s had a good review of Target and Walmart earnings. Target stock surged after earnings that beat deeply negative expectations even as its revenue was light and comparable sales fell 4.6% in its fiscal third quarter. Its outlook for the key holiday fourth quarter was roughly in line with Wall Street estimates. And they highlighted weaker consumers.

Overall, consumers are still spending, but pressures like higher interest rates, the resumption of student loan repayments, increased credit card debt and reduced savings rates, have left them with less discretionary income, forcing them to make trade-offs in their family budgets

Walmart – Walmart is the biggest retailer in the country so its results matter. And they were not as well received as Target. Walmart slid 7% with a surprise guidance cut. Walmart had run up for months into earnings. The retailer’s earnings per share beat by a penny on in-line revenue and a 4.9% increase in comparable sales. It though guidance was raised, it was below the Street’s estimates. Blame expectations on weak consumers.

We see our customers showing ongoing discretion and making trade-offs to be able to afford the things they want, given the sustained high cost of the things they need.

BJs – The store shifted from inflation to deflation concerns. A decline in prices of goods hit the top line forecast with shares plummeting 5%. The CEO stated, “We experienced more disinflation during the quarter than we expected particularly in our perishable food business.” Meaning prices that consumers are willing to pay are dropping. Plus “waning government aid has been a strain on lower income members this year”

Bipolar Consumers or Does Michigan Need Sunshine?

Given some of these retail reports and increasing US debt, many investor concern is raised. Cautious market observers are pointing out that financial stress is building up as consumer debt is growing, lending is contracting, and consumer sentiment is falling.

The concern makes sense. Just as inflation is a self-feeding mechanism – high prices expectations lead to higher pricing reality – deflation and recession is self-feeding as pessimism hits a certain point. Consumer expectations of tougher times will lead to a contraction in spending which will lead to tougher times.

One way to measure expectations is the the Michigan Consumer Sentiment Index. The Michigan Consumer Sentiment is a monthly indicator of consumer attitudes towards the national economy. It breaks down consumer sentiment into areas such as personal finances, work outlook, and overall purchasing intentions. The data is collected from a nationally representative sample of the Michigan population. It has not recovered since COVID and hit a new low this year.

One has to wonder if these companies are using consumer fears to lower future expectations. Black Friday and Cyber Monday sales show anything but a weak consumer as sales are up. Black Friday generated $9.8 billion in U.S. online sales, according to Adobe Analytics, up 7.5% from a year ago. U.S. shoppers spent $12.4 billion on Cyber Monday, a record result demonstrating the continued resilience of consumers.

Consumer sentiment is a poor indicator of short-term consumer spending behavior. Consumers whisper in fear about the future but their wallets are screaming buy, buy, buy! Or maybe Michigan needs more happiness!

How Weak Can It Be When Jobs Are So Strong?

Future spending plans are built off of inflation expectations and our ability to generate more income. Even though the price data says inflation is slowing, no one I know thinks it will. I certainly don’t think Disneyland or airline tickets are getting any cheaper (I keep praying but it doesn’t happen).

If I think prices will go up next year, I am likely to buy more stuff now before it gets more expensive (as long as I think I an afford it). Plus, people expect deals this time of year so they might be splurging now. We will come back to this.

In a consumer economy, if I believe income can be generated in the future to pay for goods, why delay gratification or needs now. Indeed, unemployment claims are low, especially in the service sector. If this keeps up, a recession just can’t happen with a strong jobs environment and continued income for consumers to service debt obligations and keep spending. We will eventually catch up with our debts, right?

What This Means For Your Portfolio in December

First an important Fed development this week.

Christopher Waller, one of the Fed’s most hawkish policymakers, signaled that interest rates were unlikely to rise further and could be cut. Waller told the American Enterprise Institute think-tank.

“I am increasingly confident that policy is currently well positioned to slow the economy and get inflation back to [the Fed’s target of] 2 per cent,”

“If we see disinflation continuing for several more months — I don’t know how long that might be, three months, four months, five months . . . you could then start lowering the policy rate just because inflation’s lower.”

Equity market rose and bond yields fell on the day with this new. Interest rate forecasts have shifted dramatically in the last few weeks.

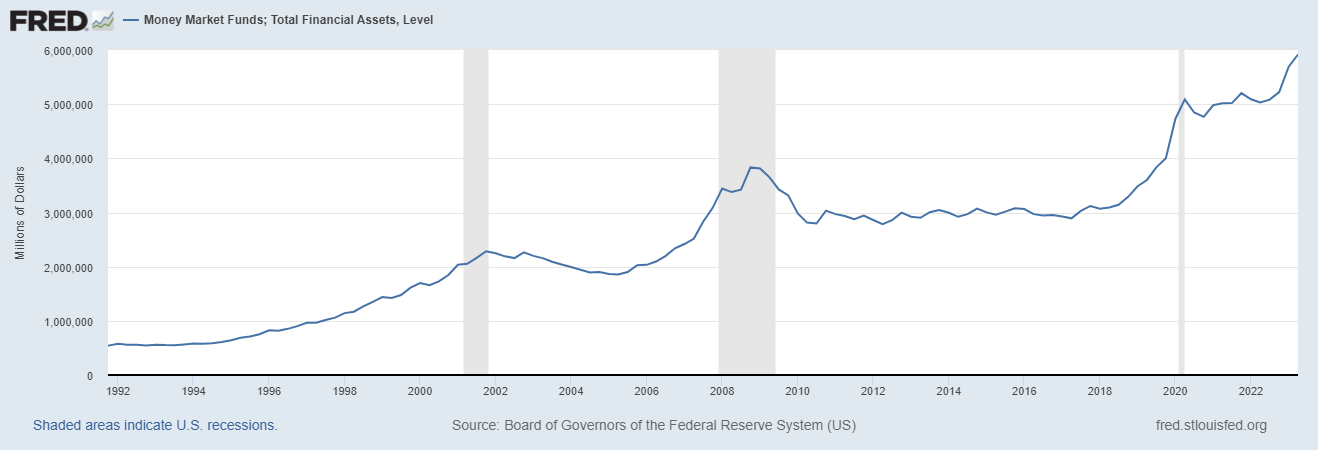

Let’s talk about the biggest source of buying pressure. Now there are massive pools of money splashing around in money market funds. They piled in last year with expectations of higher rates. As expectations of lower rates get baked in, you will hear the swish of this money emptying from money markets into rallying equities.

Then there is the lack of selling pressure. Whoever bought the leading stocks of this year (like the Magnificent 71), is sitting on large gains. No one wants to incur taxable gains in 2023. These stocks are not getting sold. With earnings out of the way and yields heading down, there is really no reason to sell.

All this points in one direction for now…up. Let’s talk about small caps, major indices, gold, and Bitcoin.

Small Saps to Rising Small Caps!

Small caps could have a 10% run ahead. It is a very popular call right now because it makes sense. If the markets are rising on falling interest rates, then small caps stand to gain the most.

Small caps have been crushed as the higher-for-longer narrative gained steam. They lag the major indices by the largest amount for 25 years.

Blame stubborn interest rates. Small caps have more volatile businesses with less reliable cash flows. As such, they have to pay less favorable terms on debt with volatile interest costs. With two-thirds of small caps having debt maturing in 5 years investors have been concerned of this refinancing cliff.

The valuations of small caps have ricocheted up and down over the last 2 years with the ebb and flow of concerns around debt and economic strength. For the short term, small caps have received a reprieve and are headed back into range.

Rotation in the Market Majors With March Higher

Just like small caps, the leading S&P sectors from Nov14-Nov24 were the most interest rate sensitive sectors.

The large indices are not driven by brick and mortar retail firms, so negative retail sentiment has little impact. Technology innovations, large and sustainable businesses, and the macro environment matters more than anything else for the major indices. As far as Wall Street is concerned there is no need to buy insurance protection for potential selloffs.

Seasonality is also a source of market strength right now. Historically speaking the 3rd year of a presidential cycle (2023 for us) is also very bullish when the rest of the year has been bullish. Strong Novembers generally lead to strong Decembers as well based on 100 years of seasonality patterns.

Gold Regains Its Shine

Gold tends to rise not in periods of inflation but in periods of perceived government mishandling and poor policy. That is why it rose post 2008 as the government flooded the market with easy money and peaked after S&P downgraded US debt in Aug 2011..

From 2011 to COVID, gold (and silver) was a dead asset. It jolted back to life for a brief while and is now nearing all time highs. When investors can’t trust the government, then in “Gold We Trust” — which also means silver future, silver companies, and gold companies will rise. What I have seen about all-time highs is that they are psychological barriers. When they are breached, the price can rocket up higher than anyone exptcts.

Bitcoin Bounces Back

Bitcoin, aka Millennial gold, has the same anti-institutional angst tied to it. I spent some time working in crypto and this is still a major rallying cry and one of the primary reason for the birth of Bitcoin. The few bitcoin related companies are all rising on this thesis - Marathon Digital Holdings, Coinbase, Microstrategy, and Riot Platforms.

The crypto scene has been cleaned up with the removal of two major bad actors this year — SBF at FTX and CZ of Binance. This purge opens the door for image conscious Wall St firms and wealth managers to build crypto friendly products for the masses.

If Bitcoin can breach $40,000 this year, we can see it approach $48,000 in the next 6 months.

Just In Case You Are Feeling Safe: How It Can All Go Wrong

A healthy dose of paranoia is key to your survival in life and investing. I leave you with a question to keep in mind. Is the market dislocated from a longer term reality? Stay paranoid and keep your eyes open to this.

There are 2 things underpinning this latest rally: lower Fed rates in the future and a strong consumer to prop up earnings. The case for lower rates is now abundantly clear.

But no one has a great explanation for robust consumer spending. There has been discussions of dwindling savings and the strapped consumer all year. Much of the consensus now is that forecasters are all wrong, no one understands the power of the consumer, and the consumer is fine as long as we have a strong job market. In other, let’s just blindly accept that the consumer is strong and focus on something else.

But what if the consumer is taking on more leverage (debt) based on a rosy view of the future earnings potential? In other words, what if they are overoptimistic about how long they can kick the proverbial can down the road?

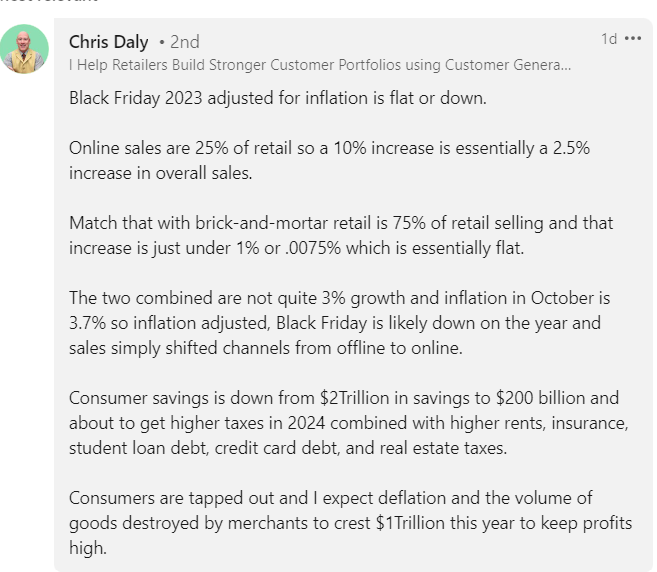

Here is a stat to give you pause. Some $79 million in sales were also made through a “Buy Now, Pay Later” plan, up 47% from last year. Buy now, pay later (BNPL) is a financing technique where a customer can purchase a product or service immediately and pay for it in installments over a specified period of time, usually with no interest charged

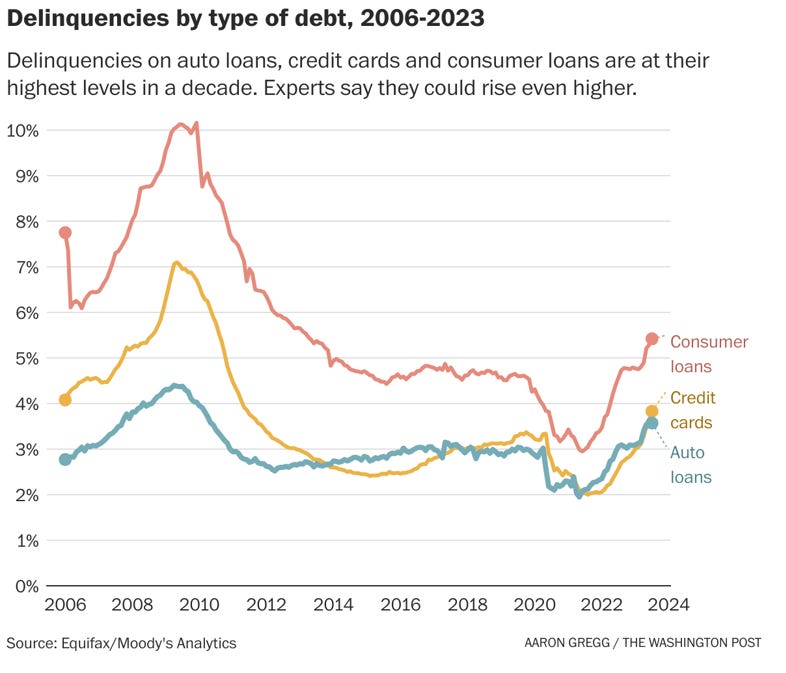

This is on top of maxing out credit cards and pulling out from 401Ks! So how much more will consumers afford in 2024? Delinquencies are rising on all types of debt and are above pre-COVID levels.

A retailer professional posted some very cogent arguments on LinkedIn (this is part of my longer conversation with him):

Bill Ackman, the legendary hedge fund manager of Pershing Square who has been spot on with macro this year, fears the consumers will put brakes faster than the Fed can cut rates. He shared in an interview:

“I think there’s a real risk of a hard landing if the Fed doesn’t start cutting rates pretty soon”

So what do you do? When there is a flood of money coming in now to bid up assets but the economy clearly is running at an unsustainable rate.

There is still a bright future for companies and assets that solve humanity’s problems. It is now more important than ever to invest for the long term in businesses and assets that have a likelihood for providing value.

Chasing the latest fads in a world of tight money is the road to ruin for the majority. Wealth will move from the hands of the impatient to the patient. Invest boldly but wisely.

If you have any questions, leave a comment. Thanks for reading Embrace the Chaos! Sharing perspective that makes sense.

Much effort and research went into making this 11-minute read. If you found it valuable, please help me out by clicking the like button ❤️ and sharing this article.

- Vikas Kalra, CFA

Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla