Treat and Then Trick. The Storms We Ignore.

Sorry, Taylor, Beyonce, and Barbie can't help.

TLDR - The markets will likely calm down in the next 2 weeks. The recession is still lurking but closing in. Unique to this time in history, business and consumers still have pandemic cash and no longer need to rely on the Fed backed banking system.

“The joy of writing about markets is the struggle to piece together a puzzle with moving parts. Often they neatly fit together. Right now, not so much.”

James MacKintosh of WSJ, Sept 2023

Hi everyone. I am back. The economy and the markets are large, complicated systems and I have been spending the last few weeks making sense of all the puzzle pieces.

It has been a tricky September. The news has been fast and furious with tweet updates, fear outbursts, and conjectures whizzing across screens. The upcoming earnings season is ripe with speculation. It is a wild card for everyone (I personally think it will be more trick than treat but I am still gathering data).

But. Even if we can’t align all of the pieces of the puzzle, certain truths are self-evident — if you don’t want to stick your head in the sand. Difficulty sits at the horizon. The storm clouds: Higher interest rates. More debt. The reliable failings of human psychology.

These will sweep down on the economy next year. Taylor Swift, Barbie, and Beyonce aren’t going to save us.

But first, what happens now? A Halloween treat, with the recent downdrafts close to ending. The storm is some ways off for reasons unique to this time in history. We will start with now and then look to the horizon.

Let’s get into it. Sections if you want to skip around:

📉Parting From Drugs Is Such Sorrow

📉5 Reasons Why The Recession Arrives Like Drying Paint

📉The Shock and Reality

Calm Before The Storm

A few weeks back I mentioned the markets might ricochet down after the Fed meeting is pinpointed with the blue arrow. And did they ever (I initially thought the strong inflation number before that meeting but timing these things is an imperfect art).

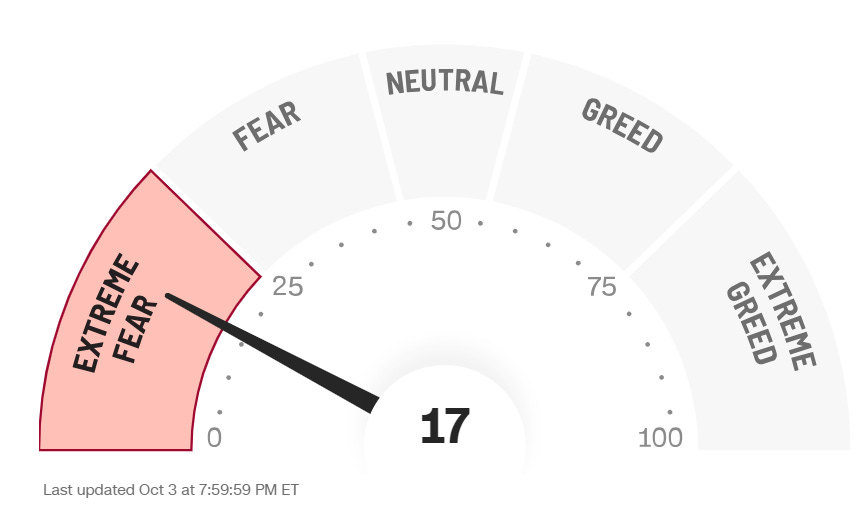

We are at a point where the market maybe oversold and could bounce back or stop going down over the next few weeks. Why? Four reasons - fear, fear, fear, and earnings.

FEAR. If you look at the charts above, the S&P 500 is falling down to the 200 EMA. After spending a few weeks here in March, the S&P stabilized.

The 200 EMA is psychological significant. Consider it the line of deep fear and also one watched by all investors. Investors can only stay scared for so long. Without a major catalyst to pull everything down, this intense selling pressure will burn itself out.

FEAR. There are many popular sentiment measures illustrating how oversold the market is and how quickly. The CNN greed and fear index is a composite of different measures and shows the market in a state of fear.

Plotting this over time, the was negative in March and last October. After both these months, the market stopped falling.

FEAR. The internet is chock full of record stock sell-off stats from bank trading desks and other market watchers. These extraordinary bouts of sentiment usually mark short-term bottoms and tops.

EARNINGS - Selling pressure tends to abate right before earnings as institutional investors switch from the hyperbole of emotion-induced predictions (fear/greed) to incorporating reality via new data (earnings).

This part of the puzzle shows at least a few weeks of calm returning. And then everyone shifts to earnings.

Parting From Drugs Is Such Sorrow

What earnings brings is anyone’s guess and is not the focus of this article. Earnings will come and go but high Fed rates/treasury rates are here to stay.

When do we come back down from the rates stratosphere? Don’t hold your breath. The market is wishing by the end of 2024. Start getting used to longer.

Low rates and easy money destroy financial health and prosperity. Financial sugar-crack pumped into the veins of the economy. Like my toddler after a sugar high, sugar-addled investors are going through low rates separation anxiety.

A historical truth. 5% rates are normal! We were living in low-rate bubble fantasy. The rates we experienced were an all-time low in the history of the United States.

These are the lowest rates we had in 5,000 years! Through the history of human existence money always had a cost.

It seemed for some time that the internet, tech, VCs, and money printing governments could levitate the markets and the economy.

But gravity never went away and always win. Investors and businesses really do miss floating on cloud nine.

The Descent to Reality

Rates are again a feature of the investing world. I know. Reality bites. Let’s talk about the end state and then how long it might take.

At some point next year the economy will sputter. Inflation will continue to eat away at savings and profitability. Disappearing savings will crimp consumer spending and the reduction in profitability will dent company investments (capital expenditures). Inefficient businesses will fall into bankruptcies.

The Writing on the Wall

This will make a slowdown (recession or stagflation) inevitable. Behavior is the biggest culprit here. People can’t change and rates aren’t coming down. Human behavior and habits are always anchored to the recent past. People and businesses (run by people) are still dreaming of abundant money and ignoring what is in front of us.

The signs are there for us to read.

First, investors and VCs. The slides below are from a market strategy deck that the famed VC firm Sequoia recently shared with its companies.

The first slide is clear, it is a RISK OFF market. Meaning stories aren’t enough. Financials and value are king. The second slide anchors the future in reality, putting the customer first, and here is a novel idea - pursue profits! But profits are hard (so cry many)!

Second, Companies.

The corporate washout is coming but it will arrive in waves. I wouldn’t expect a large 2008 credit event. The excesses in the system are spread out and for reasons we will discuss there are buffers.

Inflation is a self-reinforcing phenomenon. Goods prices went up. Now wages are going up (strikes). Companies will try to charge more because their margins are getting squeezed. Until consumers get fed up and find ways to pay less. And on and on it will go.

Consider this. Dollar General and DollarTree are losing market share to cheaper alternative Temu (owned by Pinduoduo). The first wave of bankruptcies have started and more are to follow.

Third, Consumers.

My lunch in NYC that used to cost $11 will never go below $15. Insurance costs more. Student loans are back on. Real wages (wage minus inflation) are declining for most people.

But people can’t stop spending money they don’t have. In some cases survival demands they spend money they don’t have.

In either case, auto loan delinquencies and credit card delinquencies are rising (previous chart).

All this spending of money we don’t have and have less of, is causing a quick depletion of consumer savings.

Rates Will Rise

As for rates, the Fed is not cutting rates anytime soon. Something big will need to break. The pain that is piling up is not enough to change course.

Interest rates rose last year because of the Fed but that is that not the only reason. Interest rates have been zooming last month for more ominous reasons. The rise in the federal deficit for one. The limping government and the Congressional Circus are in no position to help.

Lack of bond buying from China, our own Treasury, and other international buyers is another. Before they were safe-keeping their extra savings. Now, they have less savings and bonds have been more dangerous than crypto!

Bottom line: Interest rates are rising and the Fed can’t do anything about it. And they don’t want to. They want to crush inflation, not reduce rates.

Look at the chart below of the fed rate and inflation in the 1970s. There are 2 spikes of inflation, one in the mid 70s and another in the late 70s.

If you look carefully, in the first spike, the Fed reduced interest rates before inflation bottomed. And they declared victory. Then inflation climbed even higher in a second late 70s spike. The second time around, the Fed pulled the interest rate bazooka to tame the inflation beast. The Fed rate was raised to nearly 20% and stayed higher for longer even when inflation came down (Fed rate at 10% even when inflation was at 5%).

5 Reasons For A Delayed Recession

But people and the markets have been singing the soft-landing, Goldilocks song waiting for the Fed to lower rates. They see a perfectly engineered slowdown, nothing to worry about. I do feel like the boy who cried wolf when talking about THE recession. It seems to never come.

There are 5 good structural reasons why it is taking so long this time around. And they all boil down to a common theme: people and businesses don’t need money from banks as much as they did before.

Mortgages - A large majority of homeowners have low fixed rate mortgages and a rise in interest rates is not going to impact their cash flow. Many of us are what we would call interest rate insensitive.

Cheap Corporate Debt - Corporations take on their debt through bonds they issue. They issued a tremendous amount bonds at low rates. They have enough money until next year.

Corporate Debt Via Shadow Banking - When corporations do need cash, they don’t need to run to the banks. There is a restriction in lending in the banking system. BUT not in the economy. Apollo, Blackstone, and others are happy to lend out to Main Street and large corporations.

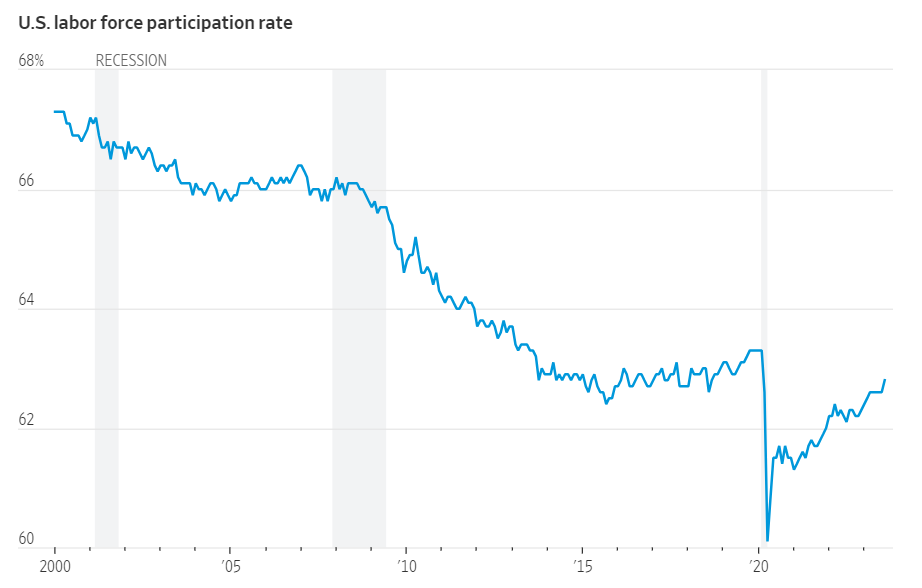

Not Enough Willing Workers - The labor market is still tight. We have less workers to fill more job. We have less immigrants. And Boomers are the largest generation in the workforce. As they leave they are not enough younger workers willing to replace them.

The economic opportunity in the digital economy now competes for labor. People have the perception that emancipation from the 9-to-5 with a successful online enabled business is available to everyone. This perception and rising inflation are causing strikes. Add this all up and the willing % of workers working is the lowest in 20+ year low.

The Consumer Is The Key

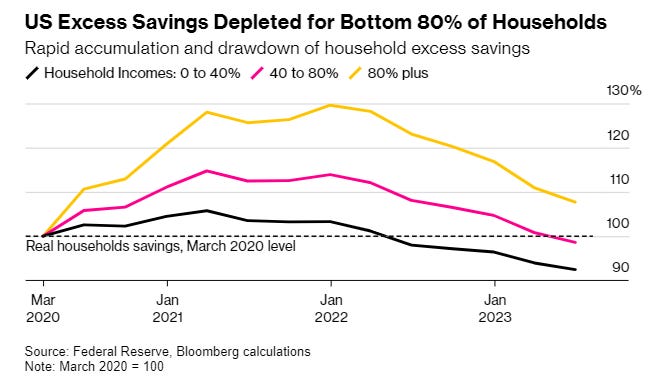

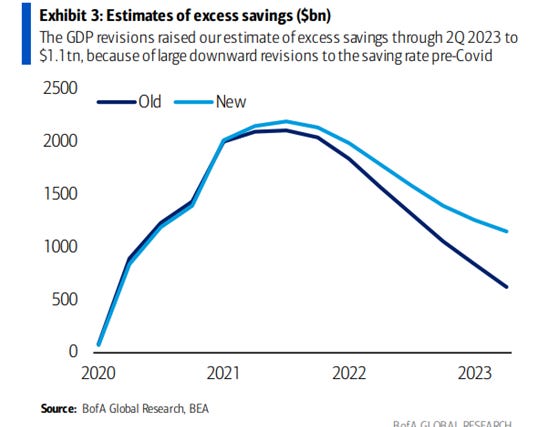

The consumer is the 5th and largest reason as they account for 70% of the economy. On the FOMC meeting, the Fed was frustrated by the strength of consumer spending. And new GDP data came out that consumers have more money than anticipated.

Even though consumer debt levels are high, they have gone up with income (see below). Consumers as a whole just aren’t strapped for cash, YET. One issue with this observation is that the people that have the money (top 20% of the households) are not the same people with higher debt (the bottom 40% of the households). There is some overlap but not as much as observers are hoping.

We are still all-in on concerts, movies, and travel because there is a dying need to reclaim normality. But that just won’t be sustainable enough to drive the economy.

I include an excellent article on the strapped consumer from my friend Geo Chen (this guys knows what he is talking about, having run a FX desk at a major bank).

Jobs are getting harder to find. Target and other major retailers are noting consumers spend is declining on goods. Student payment and credit card debt is increasing along with the cost of that debt.

As consumers deplete their wealth, the economic growth engine will slow and impact jobs and the income potential for businesses.

The storm clouds are gathering there on the horizon.

The Shock and The Recovery

If the economy were a patient, it’s health is compromised. It can trudge along fine for longer than expected but if it receives any shock from within or from the storm, the patient will suddenly get very sick.

A shock is an unknown by definition. We can’t prepare for it exactly. But if we were wiser as a society we could take safety measure like save money, spend less and do without excess.

But we aren’t. What people are failing to consider is that even though they can’t see it clearly, danger is still lurking.

“We have a very strong economy, but don’t confuse today with tomorrow”

Jamie Dimon at the Detroit Economic Club, Sept 20, 2023

In the context of the bigger picture, a period of weakness is a normal cycle in any healthy economy. Any economy that has survived has flushed out the fat and excess from time to time.

I leave you with the words of Charlie Munger of Berkshire Hathaway.

Nothing is the end. Everything that happens to society is adjustments. Adjustments can take longer than anyone expects or wants even when they take some time in arriving.

But humans adjust eventually and thrive. We always have.

If you have any questions, leave a comment. Thanks for reading Embrace the Chaos! Sharing perspective that makes sense.

Much effort and research went into making this 9-minute read. If you found it valuable, please help me out by clicking the like button and sharing this article.

- Vikas Kalra, CFA

Your articles are so educational, I wait for the next week article. Thanks