Is It Worth Breaking the Economy?

Inflation is down. Will the Fed leave it alone?

What is more damaging: a little bit of inflation or punishing the US economy?

With the latest data last week, the question now is no longer will the Fed reduce inflation. We are almost there. There being the Fed inflation target of 2%.

One after another experts and economists think the Fed has done enough:

Rick Rieder, BlackRock Inc.’s chief investment officer of global fixed income, said last week that the path to 2% inflation could bring pain to millions of workers, a trade-off that “doesn’t make sense.” Others are following along.

Mohamed El-Erian, chief economic adviser at Allianz SE, who was very skeptical of Fed policy wrote, “You cannot get in the way right now of the soft-landing narrative — that narrative is building momentum.”

Bill Dudley, senior research scholar at Princeton University’s Center for Economic Policy Studies, and hedge funds like Bridgewater Associates think that this is the end of the hiking cycle. Now everyone is expecting one more rate increase in July and no more for the year.

So what does this mean for markets?

🎉Winners: Small caps, technology, bonds, emerging markets. Lower rates are generally better for all assets but these should do especially well.

🤔Maybe Winners: Commodities - oil, gold, copper.

Let’s start with why last week was important and talk about the almighty dollar first.

Why Last Week Was Important

CPI: Consumer Inflation

CPI declined to 3% versus 4% expected. Core CPI also decreased more than expected.

Core CPI is important. Just a reminder, Core CPI is Consumer Price Index (CPI) minus food and energy. Core inflation excludes these items because their prices are more volatile. Economists believe this exclusion makes the core inflation rate more accurate by moving away the wild swings of energy and food.

This has everyone excited. Here is why:

CPI has been decreasing for months now. This is a clear and strong trend in the right direction. The argument goes that the Fed has enough evidence to let the trend play out.

We are almost at 2%. If we leave rates alone, we have the momentum to get close.

The Fed is laser focused on core inflation and it is at a level close to Nov 2021. It is clearly becoming less “sticky”.

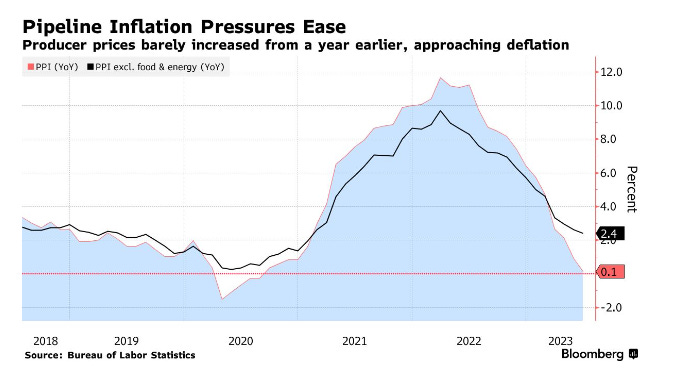

PPI: Business Inflation

The producer price index monitors the basket of prices businesses pay for their inputs. Not only is this decreasing (meaning the prices of are increasing less year over year) but one measure is approaching deflation (prices are decreasing).

Let’s take a moment to let that sink in. Prices are decreasing.

Look at the red line in the chart below. It is always a positive number (except for COVID). That means even before COVID, expenses for the same things at a business increased a little every year. CPI was the same so consumers paid slightly higher prices every year. Now prices are close to decreasing for the first time since 2020!

If we remove food and energy they are still increasing 2% YoY (year over year) but that is much better than 10%! 10% was in 2022 and that is not fun for anyone.

The 2% increase in PPI is tied to wages in the services sector. They are still sticky as there just aren’t enough workers to meet demand. But for a few months now, this has started heading in the right direction (meaning down).

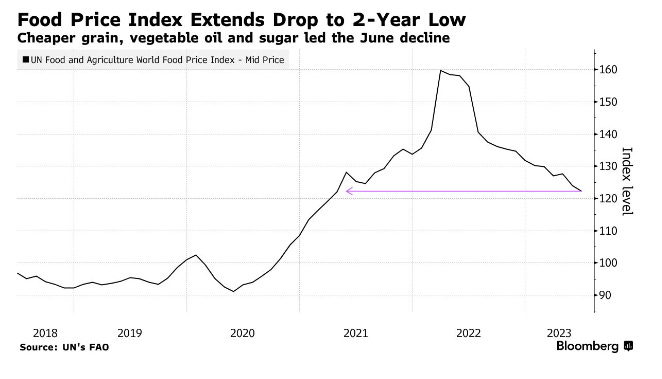

These prices are not just dropping in the US. The international food price index has dropped 25% since the high of last year. A better perspective - the index has shed 67% of food price increases since COVID started.

How long does this feel good story remain true? Investors are betting for the rest of the year. I am not sure anyone knows for sure. All forecasts are made to be broken as we have seen this year.

When The US Dollar Crashes Loudly

These expectations has caused the US dollar to plummet last week against all major currencies.

The US Dollar Index, also known as DXY, is a leading benchmark for the value of the US dollar against a basket of other major currencies. We breached 100 on the DXY. Why is this important?

100 became an important psychological level during COVID when the dollar index popped to this level and then dropped to new lows. In 2022, Fed interest rate hike momentum drove interest rates higher and higher. The DXY ripped up to 114 last year. We have flirted with 100 all of 2023 and now cracked the level.

What Happens Next?

Oil + Energy + Commodities

WTI (light sweet crude) has come down a long way from $124/barrel! After collapsing to the mid 60s earlier this year, WTI is in the mid 70s. Since March 2023 oil has been stuck in a range as the world considers oversupply, supply disruptions, travel rebound, and China reopening. Even with a strong week, we are stuck in the same range for oil.

Remember also that all commodities and risk assets gain with USD weakness. The dollar crashed. So how much is oil going up because 1) cheaper dollars means more dollars for a barrel and/or 2) a fundamentally better story (more demand than supply) for oil. This week will provide a good answer.

Bonds - The opposite of Silicon Valley Bank

After Fed rate cycles the current value of bonds rise as future bond issues are expected to provide lower yields and are less valuable. If I have a treasury bond paying 5% and rates decrease in the future to 4%, my 5% bond is more valuable.

This is the opposite of what happened with the bonds in Silicon Valley’s portfolio.

This could produce a virtuous cycle of returns as more money in bonds reduces interest rates and lower rates improve growth forecasts and improved growth forecasts drive up stock and bond returns.

Earnings + Equities

On one hand, S&P 500 firms are expected to report a 7.1% decline in earnings compared with the same quarter last year, according to the latest blended estimate from FactSet that incorporates results from firms that have already reported.

On the other hand, with a low bar, firms could outperform. Tailwinds include a crashing dollar and lower PPI. With a weaker dollar international firms will have better pricing power overseas. With a lower PPI, input costs for brick and mortar businesses are decreasing and will improve profit margins.

Some areas of the market that could have better earnings (that doesn’t necessarily mean improved stock prices):

Technology businesses would benefit from a lower cost of capital and cheaper money for growth. Large cap has rocketed at speeds unseen. Does it keep going up or do small/mid cap technology stocks follow the path higher?

Emerging markets and their stocks would benefit from a weaker dollar. A weaker dollar improves value of emerging market currencies. Especially important because EM countries have dollar debts so their debt burden drops.

Small Caps benefit from cheaper prices for raw materials and capital as discussed here a few weeks back.

Bank Earnings

Major banks kicked off earnings season last week. Net interest income (NII) — revenue collected from loan payments minus what depositors are paid — was higher for all.

Write-offs for loans, credit cards, or CRE are increasing. Some write-offs (recognition of potential loss) are expected but too much is a problem. We are in ok-for-now territory but this is an area to watch now.

WELLS FARGO

The San Francisco-based firm reported $13.2 billion in Net Interest Income for the three months through June, up 29% from a year ago. Executives now see Wells Fargo’s NII haul rising roughly 14% for the full year, more than the 10% jump they had earlier projected.

Deposits slumped 22% to $402 billion in the quarter while average deposit costs soared. The firm plugged that hole in part with $25 billion in borrowings from the Federal Home Loan Bank system. FHLB loans come at a high cost.

The bank reported a $1.7 billion provision for loan losses, more than analysts expected, which included a reserve build tied to office-building loans.

JP Morgan

The firm’s $41.3 billion in revenue beat analysts’ expectations, fueled by $21.8 billion in net interest income as well as a $2.7 billion gain on its First Republic purchase, according to a statement Friday.

The New York-based company raised its full-year guidance for NII, saying it now expects $87 billion, excluding its trading business, up from the $84 billion. But JPM warned this will not last.

“Consumer balance sheets remain healthy, and consumers are spending, albeit a little more slowly. Labor markets have softened somewhat, but job growth remains strong”, according to Jamie Dimon.

Trading and investment banking, while both down from a year earlier, came in ahead of analyst expectations, driven by beats in fixed-income trading and equity and debt underwriting.

Citigroup

Citi saw a 36% slump in net income to $2.9 billion. Higher credit balance, more write-offs, and higher severance were big drivers.

Higher interest rates and larger card balances set the stage for an 11% jump in revenue from US personal banking in the second quarter. That blunted the impact of a 78% surge in write-offs tied to consumer loans.

The bank’s expenses jumped 9% to $13.6 billion in the quarter, boosted by what executives had predicted would be hundreds of millions of dollars in severance costs for eliminating about 1,600 jobs, including investment bankers and traders.

Balances on Citi’s US credit cards swelled to $149 billion from a year earlier. Firmwide credit costs soared 43% to $1.8 billion, fueled by the write-offs as some cardholders fell behind, the bank said. The firm added $161 million in reserves, citing that business’s growth.

If you have any questions, leave a comment. Thanks for reading Embrace the Chaos! Sharing perspective that makes sense.

Much effort and research went into making this 8-minute read. If you found it insightful, click the like button and share this article.

Sharing and caring is the currency for the content economy.

- Vikas Kalra, CFA