Cloudy with a Chance of Earnings Sizzle: Part 1

What Is Mr. Market Thinking?

Happy Belated New Year everyone! Market trading volume is finally picking up post MLK. Volume is important because more volume means more votes and better information. With its return, the narratives for 2024 are emerging. This is the first of a two-part post to explore those narratives. The second post will cover names and sectors.

The main takeaway: A choppy market slowly heading higher with a chase for high quality names at least during earnings season (until mid-Feb).

Here are the links to jump around:

✅Where Forecasts Fail & What We Learn

✅Special 2024 Catalyst: Healthcare and Houthis

The first few weeks have been bumpy with investors coming to the sobering realization that interest rates are not a near certainty. But. Cuts will still start in December (we will cover that later). After a few stumbles and some very compelling earnings, the markets have regained their footing with the tech heavy Nasdaq hitting all time highs and the S&P 500 and Dow Jones close behind.

What is lagging are all the interest rates sensitive plays that rocketed in December. This includes small caps, biotech, and regional banks. When rates do start their trend down these will resume a rebound.

Just as noticeable in December were the flood of forecasts and predictions for 2024. Much of which are proving wrong but are still extremely helpful. Let me explain.

WHERE FORECASTS FAIL & WHAT WE LEARN

For many professional institutional investors and financial publications, it is a requirement to publish their best guesses. Many are not too bold and reflect deviations from a broader consensus (like in 2024 interest rates will get cut at some point). Plus making bold forecasts doesn’t feel so good if you get it wrong. Sprinkle in fear of a crash and highlights of geopolitical uncertainty. Pepper in some schadenfreude for those who were wrong and who close you might have been.

Voila! Market forecasts. This is not to minimize the work it takes to make these, but the process of production is similar for many. The market forecasts will have different flavors but will show the same assumptions baked in.

These assumptions lead to bias. And understanding the market bias is always helpful. It helps us figure out the blind side and flawed arguments over the next few quarters. Over the medium and longer term investor are notoriously difficult to understand as 2022 and 2023 (and every other year) has showed us.

They are still just best guesses. What they are not. A plan. All plans unravel quicker than expected. Holding too tightly to beliefs in investing leads to pain.

To quote the boxer “Iron” Mike Tyson:

“Everyone has a plan until they get punched in the mouth.”

Here is example that was cited in Bloomberg Odd Lots podcast about Why a Recession Didn’t Happen. The forecasts assumed that the Fed was the only source of funds and failed to account for the rapid growth of private credit that provided funds to the economy.

This was disrupting the Fed’s transmission mechanism of tightening the economy to rates. This was even though private credit was growing in plain sight. Investors that noticed this would have been at an advantage of seeing a recession was still in the distance.

Then there are things that worked before but that don’t work now because of structural changes in the market. Oil didn’t move with Middle East attacks because the US is not the biggest consumer and the Middle East is not the only supplier. China is a large consumer of oil and their economy is slowing and now the US and Latin America are oil exporters oversupplying the market.

Embedded in that assumption was that China would rebound because they would solve for growth when the communist regime was more focused on political control. In the end, Chinese deflation helped cool US inflation as the US still buys so many goods from China.

And the big mystery for all forecasters and economists was why did the yield-curve inversion fail as a recession indicator. There is no agreement on what has changed.

Bit by bit many of the most popular bearish forecasts last year fell apart. The opportunity was recognizing the fundamental flaws of these forecasts as the market refuted them.

Ultimately where prices head and what the market votes is the evidence we need to understand the truth.

THE TRUTH FROM FORECAST SURPRISES

So what are some truths we all learned so far in 2024? What evidence has the market lab proved?

Here so of the more important ones:

The much touted Santa Claus rally which lasts until the 2nd trading day of the year fizzled out spectacularly. Seasonal patterns are never a sure thing.

Gold has been up and down but going nowhere. Some times it seems the world is worried about the Middle East and other times investors just overlook the geopolitical risk. Gold looks stuck for a while and the Middle East seems a sideshow for investors.

Inflation is not so easy to vanquish as many suggested. We have massive disruptions to global shipping and global trade could get even more disrupted (more on that later). The implication is inflation may not get much lower. If that happens, the market will get very melancholy.

Nvidia was considered too expensive already and it just ripped to new all time highs. It seems the right players in AI still have plenty of room to run.

Energy was “bottoming” and but it still looks weak after the Saudis announced surprise cuts, global growth forecasts were cut, and the US keeps flooding the market with crude. Every daily jump in crude oil is followed by selling…the market just doesn’t see reasons to reprice yet.

Weak consumer? What weak consumer? American Eagle Outfitters, Crocs, Abercrombie and Finch, and Urban Outfitters and a growing number of retailers reporting an extremely strong holiday season.

Small caps were the belle of the December ball. So far they are the sick man of the race. The party might need a breather and investors might need more proof of economic recovery before diving into this 2023 under loved part of the market.

Boeing was slated to make a comeback until they lost doors mid-flight on Alaska Airline flights. Oh Boeing…nothing more to say!

No one truly understands inflation, it is a torturous beast. It seems most got it wrong in one way or another. Be wary of those who claim to understand. The ones who are perplexed by it, likely understand it the best.

SPECULATIVE IS NOT SO HOT

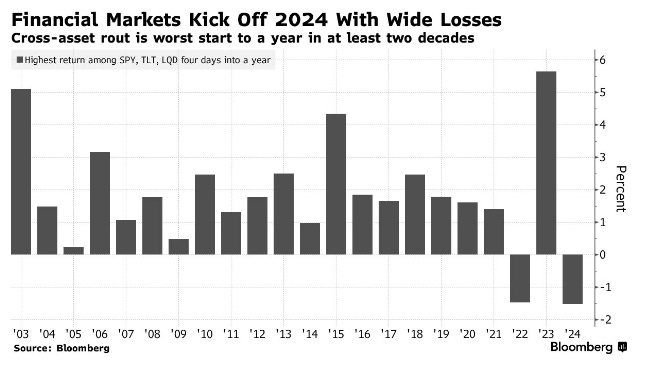

The first week started as one of the largest routs in the market in decades. We rebounded to all time highs but left some more speculative assets on stretchers.

For investors frolicking in the speculative fever at the end of the year, the year so far has been a painful dose of reality. A sample of speculative assets have all fallen 15% or more since December/November highs - Palantir, Ark Innovation, Sofi, and IPO ETF.

Lesson: Investors are seeking high quality assets in an aging bull market and an interest rate environment. That means companies that produce sales and cash.

RATES & FED RESPONSES

Jobs and inflation numbers will in part drive the Fed interest rate path. In 2024 rates have stopped their decline and this is adding volatility in the stock markets. These are the developments so far.

Jobs

While the leading indicators of demand continue to point to a slowdown, all is great on the jobs front.

December nonfarm payroll data showed that employers added 216,000 jobs, up from November’s 173,000 and better than the 170,000 economists anticipated. Services and travel/leisure are still hiring. The ratio of available jobs to available workers remains at 1.4:1, keeping upward pressure on wages.

Initial unemployment claims on Jan 18th came in at the lowest amount in one year at 187,000.

Inflation

Federal Reserve Governor Christopher Waller said the US central bank should take a cautious and systematic approach when it begins cutting interest rates.

“When the time is right to begin lowering rates, I believe it can and should be lowered methodically and carefully”, Waller said at the Brookings Institution on Tuesday.

He acknowledged inflation is cooling as seen in the previous week’s Jan CPI (consumer inflation) report which came in higher than expected.

Much of the surprise in so-called core goods, which excludes energy and food, came from pickups in prices for used cars and apparel, despite year-end promotional activity

The PPI (producer prices) came in lower than expected the day after CPI. The markets were much more jubilant with a lower PPI.

Rates & Rate Forecasts

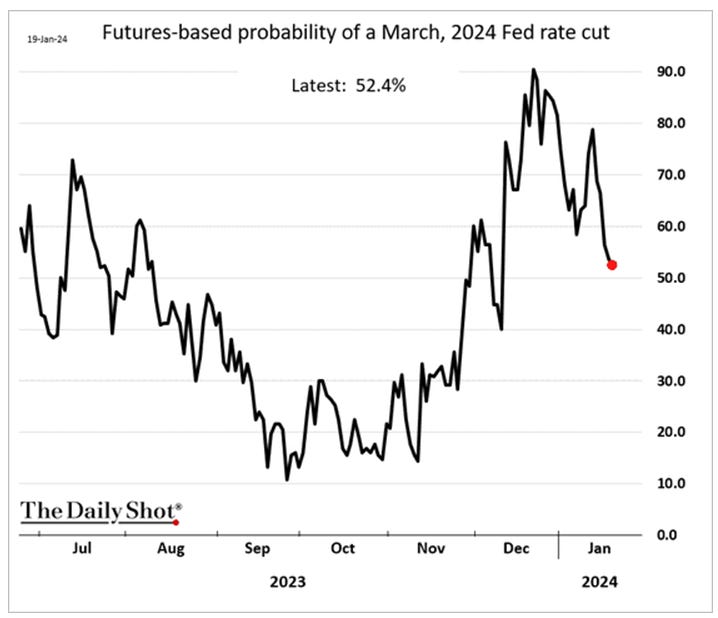

Rates were heading down into the end of 2023 but have started to creep back up to March 2023 highs.

A big part of the creep higher is that the market sobering up to the fact that the Fed is not going to increase interest rates that quickly.

Atlanta Federal Reserve President Raphael Bostic said he expects the central bank to start implementing rate cuts in the third quarter of this year.

And the market has started to listen. The probability of rate cut in March has decreased from near certainty in December to 50% as of today. ✂️

You can watch the latest changes in the Fed Fund rate here: CME FedWatch Tool - CME Group

SOFR Is Not Budging

The Secured Overnight Financing Rate (SOFR) is a benchmark interest rate that represents the cost of borrowing cash overnight collateralized by U.S. Treasury securities. It's a critical rate in the financial world, serving as a reference for various financial products, including loans, mortgages, and derivatives.

For consumers, an increase in SOFR can lead to higher interest rates on adjustable-rate mortgages (ARMs) and home equity lines of credit, escalating monthly payments and affecting household budgets. Similarly, credit card interest rates and auto loan rates may also be influenced by SOFR changes, altering the cost of consumer credit.

One interesting divergence to keep in mind, is the SOFR has not budged even though the 10-year yield dropped in 2023. There are businesses and consumers still suffering from high rates. We aren’t out of the woods yet.

SPECIAL 2024 CATALYSTS: Houthis and Healthcare

JP Morgan Health Conference

The JP Morgan Health conference is become an extremely important event for medtech, biotech, and pharmaceutical companies and investors. Odd Lots had an interesting episode reviewing the conference buzz and trends. Main takeaways:

Major focus areas included AI, GLP-1 weight loss drugs, and cancer solutions.AI is so popular that Nvidia even presented at the conference. That is right, AI is used in the drug discovery process as it uses a tremendous amount of data.

People seemed optimistic on medtech, biotech, and the funding environment after a long dry spell. It has been so bad, it will take a little but to make valuations higher.

The biotech industry is more interested in rates not rising versus absolute cuts. With the slightest hint of rate cuts, 6-7 acquisition were announced since mid Dec versus barely any in the rest of 2023. What happens when they do get announced?

Houthis, Supply Chain, and Middle East

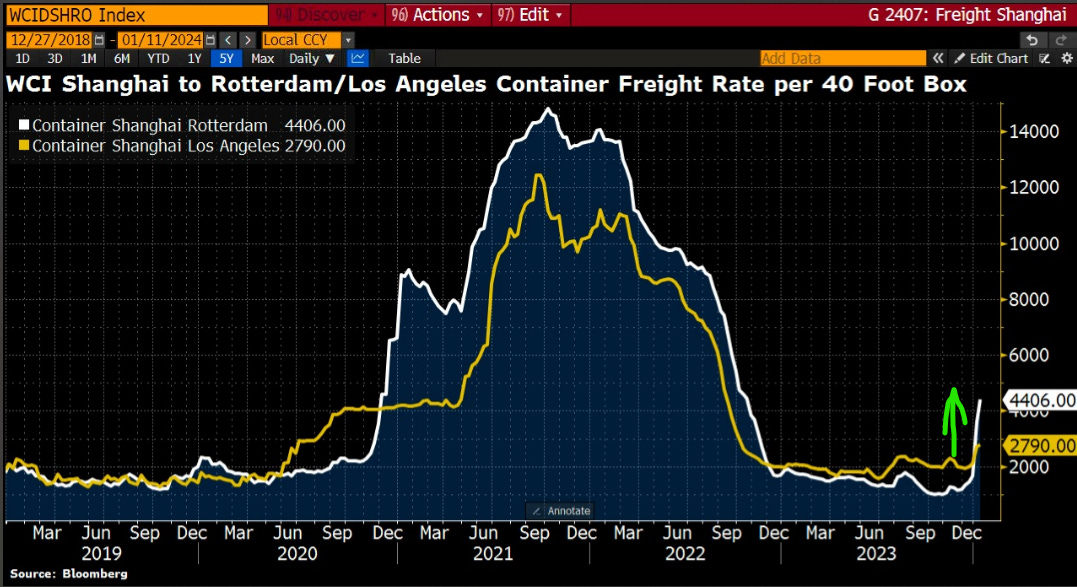

"Houthi attacks in the Red Sea spark a surge in shipping costs” or some version of that is the headline I keep seeing. The reality is for now the crisis has increased rates but they are nowhere near a concerning level.

So, yes prices have spiked somewhat. And about 30% of global container ship volumes move through the Suez Canal (linking the Red and Mediterranean seas).

Prices are moving higher but in a much more muted way. According to a Inverto, a unit of BCG:

“The Red Sea is not as dangerous to global trade as the events were a few years ago”

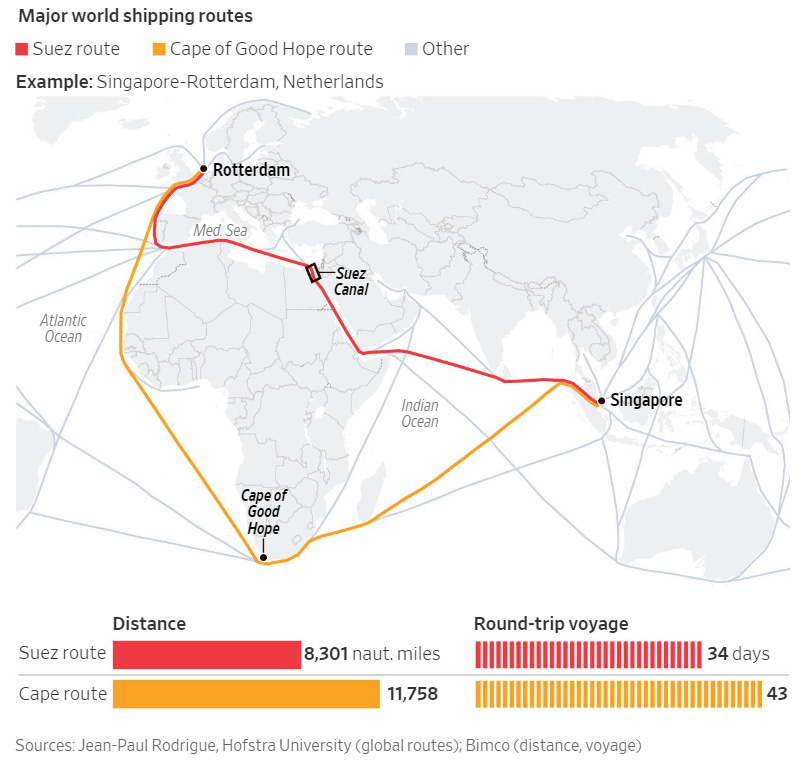

Companies have ample stock and were better prepared for global disruptions after COVID. Plus Europe is more reliant on the Suez than the US and will need to divert traffic around Africa. The US has other waterways to access markets and will likely feel an impact much later, if any.

Little impact for now. As long as no new major players get involved, the Middle East unrest will persist as background noise for the markets.

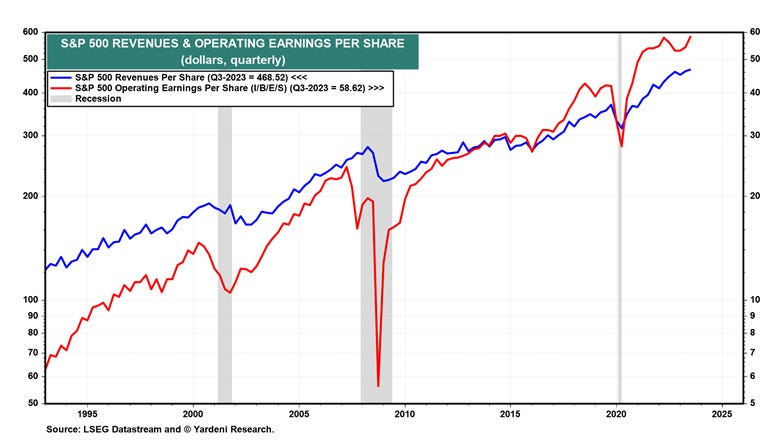

EARNINGS

Earnings took a dip in 2023 Q3 earnings season but the forecast (see red line) picked up going into our current 2023 Q4 earnings season (happening now). Banks provided less rosy earnings forecasts but some other large names have been good . In particular semiconductors, led by Taiwan Semiconductor, are showing promising earnings. Medical technology companies are generally preannouncing higher guidance.

VOLATILITY AND OTHER WORRIES

The first half of this year could continue to experience turbulence but based on some of the responses from earnings, quality firms are getting rewarded and investors are sticking with the market.

I don’t think anyone can honestly know what the second half brings. But in election years, the second half of the year is supposed to be strong. And then there is the massive wall of money in money market funds.

Once rates cuts start, this money could surge out like water from a melting glacier.

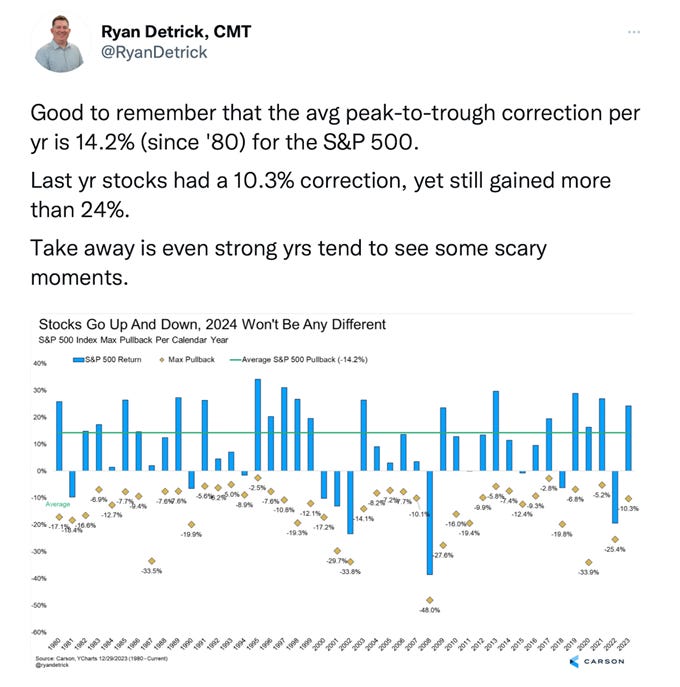

But remember. Even on good years, markets can drop 10% within the year due to the human tendency to move through cycles of fear and greed. If you are a long only passive investor hold through the volatility — volatility is the cost of investing. If you are picking individual companies, than to survive stay more conservative with how you take risk.

This year may end higher but there are going to be some uncomfortable air pockets. It is when we forget about volatility that it comes back with a painful vengeance.

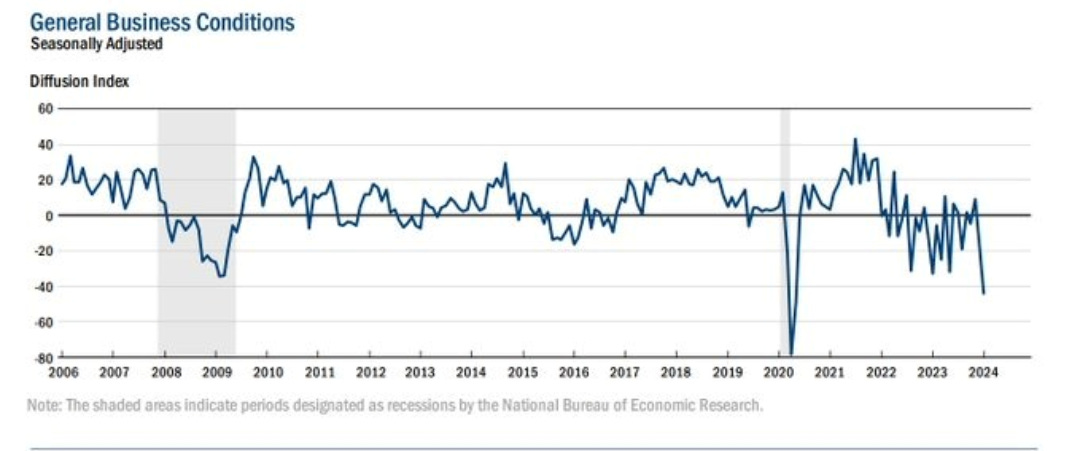

Business conditions still seem terrible by many measures. Look at the drop in general business conditions measured by the NBER and increases in bankruptcies (below). This is not showing up in the stock market yet and may not as many of these are not public firms. But the stock market is not the economy. They are related over long horizons but in the medium term the relationship is tricky as there are lags from information to flow between the two.

We are in uncharted territory because the lags are much longer than previous years. The structure of the economy has changed. Which forecasts keep ignoring and models do not capture. Outside of the Fed there is a sea of money sloshing around in the system - the massive wealth of Baby Boomers, piles of money in Private Credit, better loan terms for businesses, and when the Fed cuts rates, the trillions in money market funds.

All this may keep this party going longer than expected as long as geopolitics doesn’t sink us. We will save all of that for another day.

What does this mean for specific investment opportunities? Read Part 2 coming out shortly.

If you have any questions, leave a comment. Thanks for reading Embrace the Chaos! Sharing perspective that makes sense.

Much effort and research went into making this 12-minute read. If you found it valuable, please help me out by clicking the like button ❤️ and sharing this article.

- Vikas Kalra, CFA